News

How banks and hospitals are cashing in when patients can’t pay for health care

By: Noam Levey | Aneri Pattani | NPR

Posted on:

WASHINGTON, D.C. (NPR) — Patients at North Carolina-based Atrium Health get what looks like an enticing pitch when they go to the nonprofit hospital system’s website: a payment plan from lender AccessOne. The plans offer “easy ways to make monthly payments” on medical bills, the website says. You don’t need good credit to get a loan. Everyone is approved. Nothing is reported to credit agencies.

In Minnesota, Allina Health encourages its patients to sign up for an account with MedCredit Financial Services to “consolidate your health expenses.” In Southern California, Chino Valley Medical Center, part of the Prime Healthcare chain, touts “promotional financing options with the CareCredit credit card to help you get the care you need, when you need it.”

As Americans are overwhelmed with medical bills, patient financing is now a multibillion-dollar business, with private equity and big banks lined up to cash in when patients and their families can’t pay for care. By one estimate from research firm IBISWorld, profit margins top 29% in the patient financing industry, seven times what is considered a solid hospital margin.

Hospitals and other providers, which historically put their patients in interest-free payment plans, have welcomed the financing, signing contracts with lenders and enrolling patients in financing plans with rosy promises about convenient bills and easy payments.

For patients, the payment plans often mean something more ominous: yet more debt.

Millions of people are paying interest on these plans, on top of what they owe for medical or dental care, an investigation by KHN and NPR shows. Even with lower rates than a traditional credit card, the interest can add hundreds, even thousands of dollars to medical bills and ratchet up financial strains when patients are most vulnerable.

Robin Milcowitz, a Florida woman who found herself enrolled in an AccessOne loan at a Tampa hospital in 2018 after having a hysterectomy for ovarian cancer, said she was appalled by the financing arrangements.

“Hospitals have found yet another way to monetize our illnesses and our need for medical help,” said Milcowitz, a graphic designer. She was charged 11.5% interest — almost three times what she paid for a separate bank loan. “It’s immoral,” she said.

MedCredit’s loans to Allina patients come with 8% interest. Patients enrolled in a CareCredit card from Synchrony, the nation’s leading medical lender, face a nearly 27% interest rate if they fail to pay off their loan during a zero-interest promotional period. The high rate hits about 1 in 5 borrowers, according to the company.

For many patients, financing arrangements can be confusing, resulting in missed payments or higher interest rates than they anticipated. The loans can also deepen inequalities. Lower-income patients without the means to make large monthly payments can face higher interest rates, while wealthier patients able to shoulder bigger monthly bills can secure lower rates.

More fundamentally, pushing people into loans that threaten their financial health runs against medical providers’ first obligation to not harm their patients, said patient advocate Mark Rukavina, program director at the nonprofit Community Catalyst.

“We’re dealing with sick people, scared people, vulnerable people,” Rukavina said. “Dangling a financial services product in front of them when they’re concerned about their care doesn’t seem appropriate.”

Debt upon debt for patients, as finance firms get a cut of payments

Nationwide, about 50 million people — or 1 in 5 adults — are on a financing plan to pay off a medical or dental bill, according to a KFF poll conducted for this project. About a quarter of those borrowers are paying interest, the poll found.

Increasingly, those interest payments are going to financing companies that promise hospitals they will collect more of their medical bills in exchange for a cut.

Hospital officials defend these arrangements, citing the need to offset the cost of offering financing options to patients. Alan Wolf, a spokesperson for the University of North Carolina’s hospital system, said that the system, which reported $5.8 billion in patient revenue last year, had a “responsibility to remain financially stable to assure we can provide care to all regardless of ability to pay.” UNC Health, as it is known, has contracted since 2019 with AccessOne, a private equity-backed company that finances loans for scores of hospital systems across the country.

This partnership has had a substantial impact on patient debt, according to a KHN analysis of billing and contracting records obtained through public records requests.

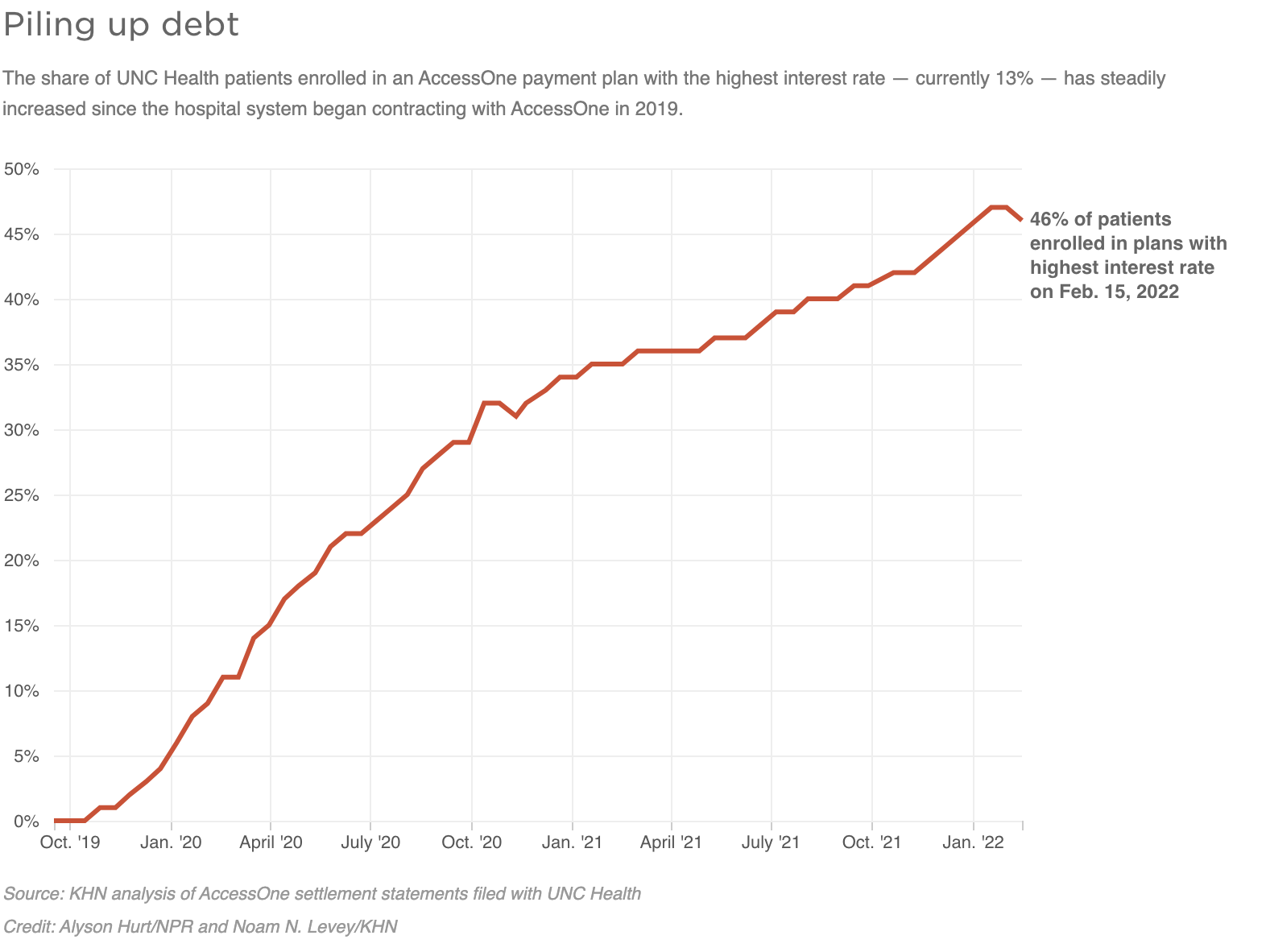

Most patients in 2019 were in no-interest payment plans

UNC Health, which as a public university system touts its commitment “to serve the people of North Carolina,” had long offered payment plans without interest. And when AccessOne took over the loans in September 2019, most patients were in no-interest plans.

That has steadily shifted as new patients enrolled in one of AccessOne’s plans, several of which have variable interest rates that now charge 13%.

In February 2020, records show, just 9% of UNC patients in an AccessOne plan were in a loan with the highest interest rate. Two years later, 46% were in such a plan. Overall, at any given time more than 100,000 UNC Health patients finance through AccessOne.

The interest can pile on debt. Someone with a $7,000 hospital bill, for example, who enrolls in a five-year financing plan at 13% interest will pay at least $2,500 more to settle that debt.

How a short-term solution ‘leads to longer-term problems’

Rukavina, the patient advocate, said adding this burden on patients makes little sense when medical debt is already creating so much hardship. “It may seem like a short-term solution, but it leads to longer-term problems,” he said. Health care debt has forced millions of Americans to cut back on food, give up their homes, and make other sacrifices, KHN found.

UNC Health disavowed responsibility for the additional debt, saying patients signed up for the higher-interest loans. “Any payment plans above zero-interest terms/conditions in place with AccessOne are in place at the request of the patient,” Wolf said in an email. UNC Health would only provide answers to written questions.

UNC Health’s patients aren’t the only ones getting routed into financing plans that require substantial interest payments.

At Atrium Health, a nonprofit system with roots as Charlotte’s public hospital that reported more than $7.5 billion in revenues last year, as many as half of patients enrolled in an AccessOne loan were in one of the company’s highest-interest plans, according to 2021 billing records analyzed by KHN.

A finance firm calls such loans ’empathetic patient financing’

AccessOne chief executive Mark Spinner, who in an interview called his firm a “compassionate, empathetic patient financing company,” said the range of interest rates gives patients and medical systems valuable options. “By offering AccessOne, you’re creating a much safer, more mission-aligned way for consumers to pay and help them stay out of medical debt,” he said. “It’s an alternative to lawsuits, legal action, and things like that.”

AccessOne, which doesn’t buy patient debt from hospitals, doesn’t run credit checks on patients to qualify them for loans. Nor will the company report patients who default to credit bureaus. The company also frequently markets the availability of zero-interest loans.

Some patients do qualify for no-interest plans, particularly if they have very low incomes. But the loans aren’t always as generous as company and hospital officials say.

AccessOne borrowers who miss payments can have their accounts returned to the hospital, which can sue them, report them to credit bureaus, or subject them to other collection actions. UNC Health refers unpaid bills to the state revenue department, which can garnish patients’ tax refunds. Atrium’s collections policy allows the hospital system to sue patients.

Because AccessOne borrowers can get low interest rates by making larger monthly payments, this financing system can also deepen inequalities. Someone who can pay $292 a month on a $7,000 hospital bill, for example, could qualify for a two-year, interest-free plan. But a patient who can pay only $159 a month would have to take a five-year plan with 13% interest, according to AccessOne.

“I see wealthier families benefiting,” said one former AccessOne employee, who asked not to be identified because she still works in the financing industry. “Lower-income families that have hardship are likely to end up with a higher overall balance due to the interest.”

Andy Talford, who oversees patient financial services at Moffitt Cancer Center in Tampa, said the hospital contracted with AccessOne to make it easier for patients to manage their medical bills. “Someone out there is helping them keep track of it,” he said.

But patients can get tripped up by the complexities of managing these plans, consumer advocates say. That’s what happened to Milcowitz, the graphic designer in Florida.

Milcowitz, 51, had set up a no-interest payment plan with Moffitt to pay off $3,000 she owed for her hysterectomy in 2017. When the medical center switched her account to AccessOne, however, she began receiving late notices, even as she kept making payments.

Only later did she figure out that AccessOne had set up two accounts, one for the cancer surgery and another for medical appointments. Her payments had been applied only to the surgery account, leaving the other past-due. She then got hit with higher interest rates. “It’s crazy,” she said.

Lenders see a growing business opportunity

While financing plans may mean more headaches and more debt for patients, they’re proving profitable for lenders.

That’s drawn the interest of private equity firms, which have bought several patient financing companies in recent years. Since 2017, AccessOne’s majority owner has been private equity investor Frontier Capital.

Synchrony, which historically marketed its CareCredit cards in patient waiting rooms, is now also inking deals with medical systems to enroll patients in loans when they go online to pay bills.

“They’re like pilot fish eating off the back of the shark,” said Jonathan Bush, a founder of Athenahealth, a health technology company that has developed electronic medical records and billing systems.

As patient bills skyrocket, hospitals face mounting pressure to collect more, which can make financing arrangements seem appealing, industry experts say. But as health systems go into business with lenders, many are reluctant to share details. Only a handful of hospitals contacted by KHN agreed to be interviewed about their contracts and what they mean for patients.

Several public systems, including Atrium and UNC Health, disclosed information only after KHN submitted public records requests. Even then, the two systems redacted key details, including how much they pay AccessOne.

AU Health, which did not redact its contract, pays AccessOne a 6% “servicing fee” on each patient loan the company administers. But like Atrium and UNC Health, AU Health refused to provide any on-the-record interviews.

Other hospital systems were even less transparent. Mercyhealth, a nonprofit with hospitals and clinics in Illinois and Wisconsin that routes its patients to CareCredit, would not discuss its lending practices. “We do not have anyone available for this,” spokesperson Therese Michels said. Allina Health and Prime Healthcare also wouldn’t talk about their patient financing deals.

Bush said there’s a reason so few hospitals want to discuss their financing deals: They’re embarrassed. “It’s like they quietly write someone’s name on a piece of paper and slide it across the table,” he said. “They don’t want to be a part of it because they have in their institutional memory that they are supposed to look after patients’ best interests.”

Some hospitals and banks still offer interest-free help

Not all hospitals expose their patients to extra costs to finance medical bills.

Lake Region Healthcare, a small nonprofit with hospitals and clinics in rural Minnesota that contracts with Missouri-based Commerce Bank, charges no interest or fees on payment plans. That’s a decision that spokesperson Katie Johnson said was made “for the benefit of our patients.”

Even some AccessOne clients such as the University of Kansas Health System shield patients from interest. But as providers look to boost their bottom lines, it’s unclear how long these protections will last. Colette Lasack, who oversees financing for the Kansas system, noted: “There’s a cost associated with that.”

Meanwhile, large national lenders such as Discover Financial Services are looking at the patient financing business.

“I’ve had to become more of a health care marketer,” said Matt Lattman, vice president for personal loans at Discover, which is pitching the loans to people with unexpected medical bills. “In a world where many people are ill prepared to cover their health care costs, the personal loan can provide an opportunity.”

KHN (Kaiser Health News) is a national, editorially independent newsroom and program of KFF (Kaiser Family Foundation).

9(MDU1ODUxOTA3MDE2MDQwNjY2NjEyM2Q3ZA000))